You’re standing at a cafe, you swipe your card, “Approved” pops up on the screen, you grab your drink and walk out. It feels fast and simple but there are actually quite a lot of entities involved in that short little interaction. When it all works it feels unimportant, but payments technology affects who we do business with, and how we do that business.

In this series on commerce technology, we’ll dive into what’s going on behind the scenes and how that affects the business you do.

Here, we walk through the credit card payment industry.

I recently had a talk with fellow payments nerd Jon Moore. While we are both very involved in the commerce tech space, we came at it from different angles. I have a background in technology doing eCommerce web development, so I’m familiar with the technical implementation of payment systems. While Jon has spent 11 years working on the business side of payments and knows all the players involved in that industry.

For someone not familiar with the payments business, there are so many questions. What exactly is an acquirer? Why can’t credit cards do micro-transactions? Who is getting what fees and when? Will cryptocurrencies impact the payments business in the states?

I spent an hour asking Jon these questions, and boiled his responses down to the below summary.

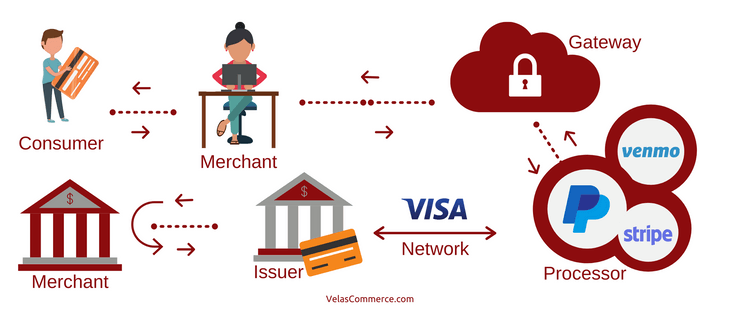

Who’s Who

Let’s dig into the who’s who, and there are quite a few people to get to know…

Players:

- Consumer: Person with a credit card, making a payment.

- Merchant: The business receiving the payment.

- Gateways: A software service that collects credit card payment information and securely transmits the data to the processor.

- Processor: Executes the transaction by transmitting data between the consumer, the merchant and the issuing bank. Examples are PayPal, Stripe, and Square.

- Network: Visa, Mastercard, etc.

- Issuer: The bank that issued the consumer card, the customers bank.

- Acquirer: The bank the money is going to, the merchants’ bank.

Payments Step by Step

Let’s walk through it from the perspective of Alice, who owns an online garden supply shop. Bob is looking to buy some nice outdoor lights for his deck. He finds just what he is looking for, adds it to the websites online shopping cart, and begins the checkout process. On an encrypted page of the website, a form pops up asking Bob for his credit card details. The payment gateway is handling this part of the process and all the credit card data will be stored in the gateways databases and not on Alice’s website. This will save her from having to worry about PCI DSS. An example of a common payment gateway is Authorize.net.

All this data is then transmitted to the payment processor. The payment processor does the work of checking that Bob does indeed have $200.00 in his bank account to cover the payment. Examples of payment processors are PayPal, Stripe, and Square.

All of this exchange of data is happening over a payment network, for example Visa’s network. And this is a physical network owned by the payment network being used.

The processor has to check in with the Issuer, the customer’s bank, and be sure that funds are indeed available. There are two processes that happen here…

Processes:

- Authorization: Takes authentication data such as pin, signature, bio-metrics, etc.

- Settlement: When the merchant actually receives the funds. This can take 1 to 3 days.

First up is the authorization process. This is where all of these systems are used to validate that the customer does have funds to make the purchase and that the issuing bank approves the purchase.

Once the transaction has been authorized, it can be “batched” and completed, or settled. However, the settlement process isn’t quite what it seems. While a transaction is generally considered “settled” and the merchant receives funds within 1–3 business days, it can take up to 6 months for the transactions to be “finalized”. The terms of service with payment network providers, Visa, Master Card, Discover and American Express, allow cardholders to dispute transactions up to 180 days after the transaction occurred. This means that for six full months, a business accepting credit card payments can lose those funds that were originally deposited into the business bank account.

Funds being removed from a merchants bank account is known as a “charge-back”. This looming possibility impacts a merchants’ behavior. They may choose not to engage in certain business activities where transactions have high charge-back rates as doing so may mean a loss of money and damage to their relationship with their bank.

All of these entities are doing business and want money flowing to the merchant, so they can collect their fees, of which there are many.

Who Pays Who?

While we know that Bob paid Alice, all the other intermediaries here have to get paid as well. When and how does that happen?

Fees:

- Issuer: Interchange fee. Paid by the merchants’ bank.

- Gateway: Monthly fee, per charge fee, chargeback fees. Paid by the merchant.

- Network: Network fee or interchange fee. Paid by the Acquirer.

- Processor: Acquirer’s margin.

- Acquirer: Processing fees. Paid by the merchant.

While all of these service providers are taking a small percentage or a small monthly fee, it really adds up. Global revenues in the payment industry reached $1.9 trillion in 2018. As we engage in more and more eCommerce, payments are a complex but growing business.

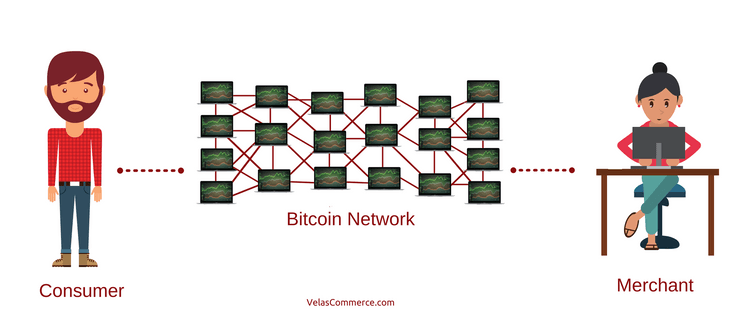

Will Crypto Impact This?

The credit card payment business is complicated! It took me a while to wrap my head around it, and when doing so you can’t help but ask, “is there an easier way to do this?” Cryptocurrencies and their associated networks offer the potential to make this so much simpler. So what would payments look like in a crypto world, and will it ever happen?

In a crypto world, yes, this process would be dramatically simpler.

Players:

- Consumer: Person making a payment.

- The chosen crypto network.

- Merchant: The business receiving the payment.

The fees involved would also look much simpler.

Fees:

- Network: Network processing fee. Paid by the sender.

Note: A huge caveat here is that crypto networks have a very big scaling problem. However, there are solutions out there that hold huge promise, particularly for payments. An example here is the Lightning Network.

So with such huge potential for simplification, why aren’t we doing this now? Well, that is a great question with a complicated answer which is the topic of an upcoming post. For the moment what we’ll say is that this isn’t that simple. The changes necessary are not just technical, but economic and would require radical business restructuring as well.

When looking at payments from mostly a technical perspective you can see the clear technical advantage that cryptos have. I’ve been envisioning a future where crypto serves as a medium of exchange, meaning that crypto is used behind the scenes as the payment network even if we are all measuring our cost(unit of account) in our local government currencies, USD, EUR, etc. Jon, however, has been looking at payments from a business perspective and offers a different possibility for the future.

Jon sees a future where crypto may serve largely as a store of value. A future where Bitcoin, Litecoin etc. are the “stable coins”, coins that hold their value very well. And in contrast, we may all be paying with fiat(USD, EUR, etc) or central bank digital currencies and settling into cryptos.

Who We Do Business With

While buying your morning Starbucks you don’t think much about that transaction. But the payment infrastructure that is being used has a big impact on what you can and can’t buy, and who you can and can’t buy from. Have you ever done business with someone outside the Visa Network’s reach? Have you had trouble donating to a politically controversial organization? Have you ever paid just 5¢ for something online? How you answered these questions will depend heavily on the payments infrastructure you’ve been using.

We’ll continue to explore these issues in upcoming editions of this series on commerce tech.

Bonus: Why Can’t We Have Micro-transactions?

Micro-transactions are interesting from both a technical and business perspective, but they aren’t happening. Why can’t/won’t credit cards facilitate them? After all, what is being transmitted are just ones and zeros logged in a database. So why not 2 or 5 cents at a time? Well, as Jon explains, this isn’t a technical problem, it’s a business problem, it’s all about the fees. A long story short, with the way that credit card fees currently work, micro-transactions don’t make economic sense. They do however make economic sense on new infrastructure such as the Lightning Network.

Resources:

The Velas 250+ link Blockchain resource page.

The Velas Commerce Crypto Commerce resource page.

1 Comment

Davidredly

Thanks, I've been looking for this for a long time